Newsletter commentary June 2023

Time:2023-07-07

Time:2023-07-07

The market in June remained challenging, but we maintained a high position and our portfolio continued under pressure. We believe that the market is overly pessimistic, and our portfolio is built on the following considerations:

First, we can rule out a Japanese-style balance sheet recession. Recently, this phrase has been very popular. As I was typing, I almost typed "balance sheet recession" and the autocomplete suggested "Japanese-style balance sheet recession". Mr. Gu Chaoming mentioned that someone told him that half of the doctoral students are writing papers on this topic. This reminds me of the continuous appreciation of the RMB since 2005-2006, when everyone was discussing whether the Chinese economy would follow the path of the Plaza Accord. The cautious economic expectations of the Chinese household sector currently causing a slowdown in debt expansion is different from the passive reduction of debt by Japanese companies and households at that time.

When the Japanese stock market peaked, its market value accounted for nearly half of the global market, with a P/E ratio of 60-70 times, far exceeding other markets' P/E ratios of 12-15 times, and a P/B ratio of 5 times. At the same time, commercial real estate increased by five times in five years. Subsequently, the stock market fell by 80% for 12 years, and house prices also fell sharply. Meanwhile, the impact was amplified by issues such as cross-shareholdings among companies, and the corporate and household sectors passively reduced their debt to improve their balance sheets.

In contrast, China's major broad-based index has a P/E ratio of just over 10 times, and while there are some issues with real estate, it is still incomparable to the situation in Japan at that time. To conduct research using analogies, there are countless dimensions that can be compared, and we can always find a few dimensions that favor our own viewpoint. The easiest to persuade are not entirely wrong, but rather appear somewhat correct. Analogizing to a Japanese-style balance sheet recession belongs to this category because it is easy to accept that the two are comparable due to factors such as housing prices and demographic changes.

The challenges encountered by the Chinese economy in the first half of the year are real, but different interpretations will have a significant impact on future expectations. Geopolitics is a complex influencing factor, but renewed communication has reduced the possibility of unexpected risks, and phased easing is still worth expecting in the second half of the year. Local debt issues have long existed, and there have been many major decisions in history specifically to address this issue, such as the replacement of special bonds. Public and transparent tightening of debt has been the main tone in recent years. This issue is not a matter of ability, but more of willingness, which will change with the situation. Unordered debt expansion is frightening, but debt is also one of the conditions for growth.

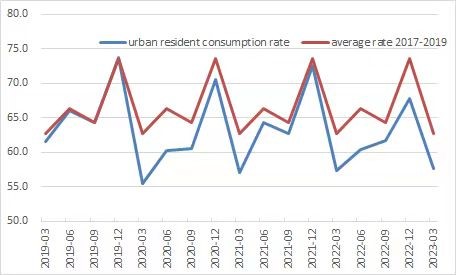

The future recovery of the Chinese economy is heavily reliant on consumption. However, consumption is insufficient in terms of the recovery drive under the restoration of scenes. We believe that the consumption rate has slightly rebounded in the first quarter, but there is still a big difference from before the epidemic. The normalization of the consumption rate is the biggest driving force for the next stage of consumption recovery. There are two key points: the recovery of service consumption and the recovery of durable goods consumption. Durable goods consumption is sensitive to interest rates, and low interest rates will be helpful. If there is policy stimulus, it will be even better.

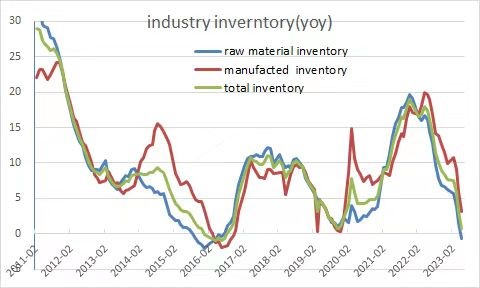

At the beginning of the year, there was a one-time release of demand that had been delayed by the epidemic, resulting in a passive decrease in inventory. However, demand was poor in April and May, and expectations also declined. Companies actively reduced their inventory, and historically, zero inventory growth is a sign of inventory reduction completion. Rebuilding inventory is helpful for both the economy and economic expectations.

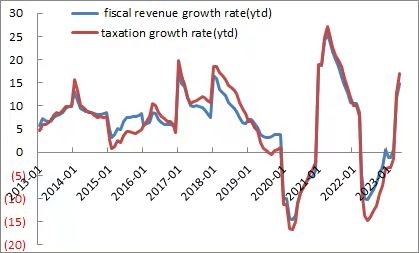

Last year, many temporary fiscal stimulus policies were introduced. With the recovery of the economy, many policies automatically expired, and the inadequate strength of the economic recovery also affected expectations. This made the effects of loose monetary policy less fully utilized, and the demand for revitalizing the economy will increase in the future. With both CPI and PPI being very low, the crowding-out effect of active fiscal policy is low, and the guidance effect will be significant. In the case of remaining resources, it is a better choice to quickly push the economy to a higher level.

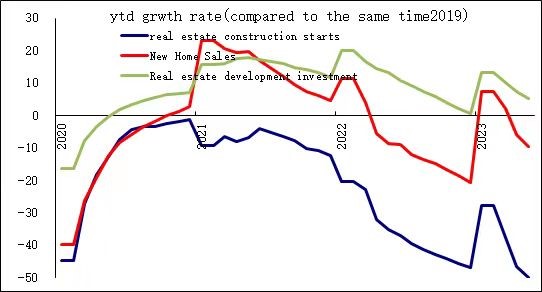

Real estate investment is a major drag. Notably from January to May this year, the new construction area decreased by 50% compared to 2019, and it has already fallen below the mid-term equilibrium sales area expectation. In the future, the drag on this part will be more due to the gradual transmission from new construction to the existing construction in progress. The pressure of a significant further decline in new construction has decreased. In addition, policy optimization targeted at the improvement demand of some cities will also help improve expectations for the real estate market.

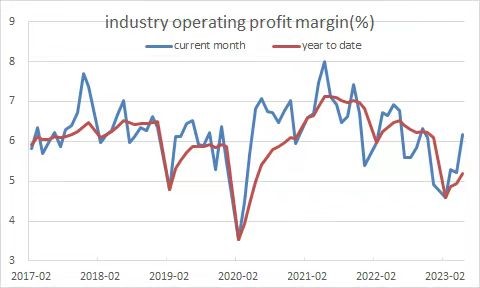

The profitability of industrial enterprises has been greatly affected in the past due to sluggish CPI and PPI. However, there are signs of improvement in the current month's operating profit margin for industrial enterprises above a certain scale.

Lastly, given the volatility of the exchange rate. The depreciation of the Chinese yuan is related to the inconsistency of domestic and foreign monetary policy cycles, and it implies that there is no self-adjustment mechanism for the domestic economy to fully utilize its potential growth rate. The exchange rate is not an unordered depreciation. In the absence of pressure on our CPI and PPI, it can be a good supplement to total demand.

Overall, the market perceives that the recovery of the Chinese economy is mixed with one-time repairs, changes in expectations, interference from inventory reduction, and the exit pace of fiscal stimulus policies, along with the decline in stock prices forming a negative cycle. We think that the economy is still slowly recovering and comparing to current market expectations and the potential help from policies, the market may be too pessimistic. Even if we are entering a period of cooling, there are still four seasons in a year. Looking forward to in the second half of the year, the phased easing of external relations, the rebuilding of inventory, the recovery of consumption rates, the return of active fiscal policies, and the rebalancing effect of the exchange rate will all have opportunities to contribute. Moreover, the judgment of entering a period of cooling may also be wrong.